Secondary Battery Market Size 2026-2030

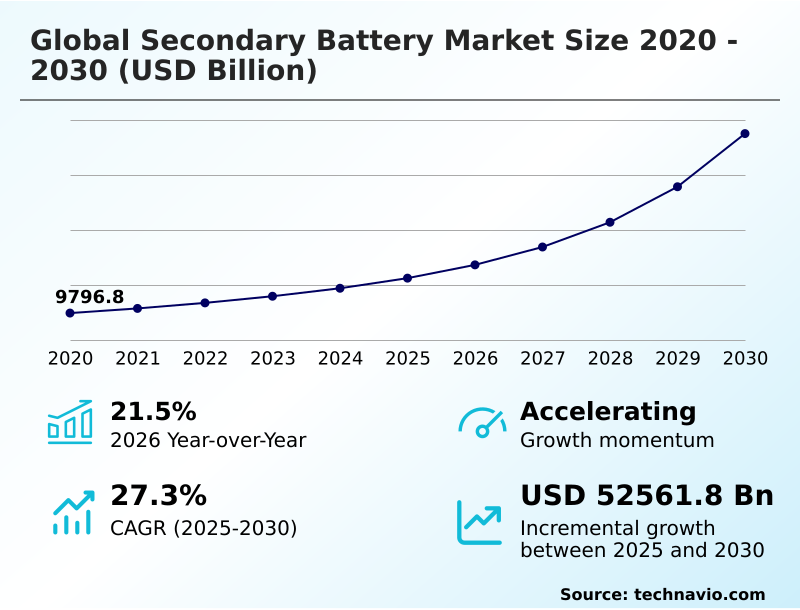

The secondary battery market size is valued to increase by USD 52561.8 billion, at a CAGR of 27.3% from 2025 to 2030. Rising demand for electric vehicles worldwide will drive the secondary battery market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 46.6% growth during the forecast period.

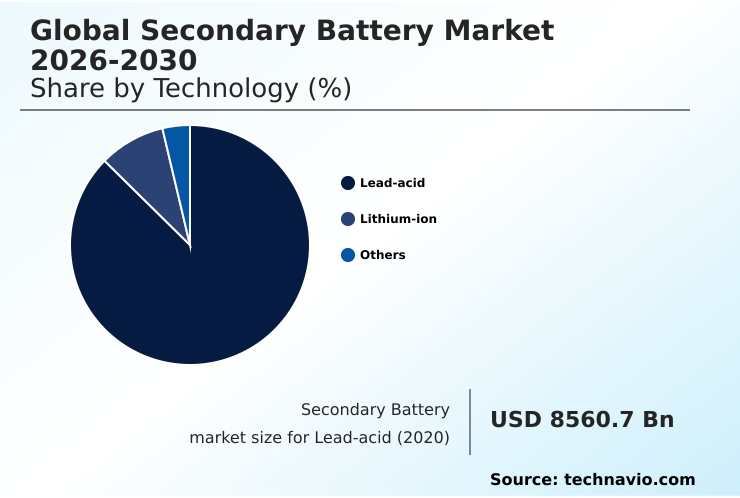

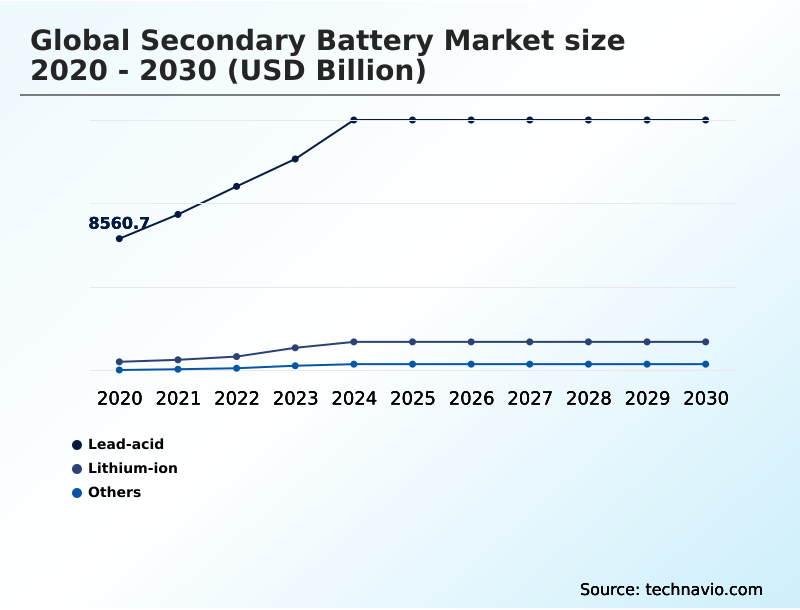

- By Technology - Lead-acid segment was valued at USD 15968.9 billion in 2024

- By Application - Automotive batteries segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 65258.6 billion

- Market Future Opportunities: USD 52561.8 billion

- CAGR from 2025 to 2030 : 27.3%

Market Summary

- The secondary battery market is undergoing a significant transformation, driven by the convergence of energy transition and technological innovation. The imperative for efficient energy storage solutions is escalating, particularly with the global push toward electric mobility and renewable energy integration.

- High energy density lithium ion batteries have become the cornerstone of this shift, powering everything from consumer electronics to large-scale battery energy storage systems that ensure grid stability.

- A key business scenario involves logistics companies transitioning their fleets to electric vehicles; this requires not just the procurement of EVs, but a strategic investment in on-site fast charging batteries and sophisticated battery management systems to minimize downtime and optimize charging schedules based on energy tariffs, thereby impacting operational budgets and sustainability reporting.

- This transition highlights the market's complexity, where performance metrics like cycle life and thermal management are as critical as the initial cost. The supply chain for these rechargeable battery systems is also evolving, with an increased focus on battery recycling and material recovery to mitigate raw material volatility.

- This circular economy approach is becoming a critical component of long-term strategy for market participants.

What will be the Size of the Secondary Battery Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Secondary Battery Market Segmented?

The secondary battery industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Technology

- Lead-acid

- Lithium-ion

- Others

- Application

- Automotive batteries

- Industrial batteries

- Portable batteries

- Others

- End-user

- Residential

- Commercial

- Industrial

- Utilities

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Technology Insights

The lead-acid segment is estimated to witness significant growth during the forecast period.

The market's segmentation reflects a diverse technological landscape where established and emerging solutions coexist.

The lead-acid battery systems segment, for instance, remains a vital component of the energy storage infrastructure, particularly for automotive lead acid batteries and industrial battery solutions requiring a reliable uninterruptible power supply.

While advanced battery technologies are gaining ground, this rechargeable battery format is critical for stationary energy storage and power grid stabilization.

Efforts are underway to improve battery reuse solutions for this segment, enhancing its sustainability profile within the broader market, where some facilities report recovery efficiencies over 90%.

The Lead-acid segment was valued at USD 15968.9 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 46.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Secondary Battery Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by dominant manufacturing hubs in APAC, which accounts for over 46% of the incremental growth. This region excels in the production of lithium ion batteries, including prismatic lithium ion batteries for automotive battery packs.

North America and Europe are rapidly expanding their domestic capacities for rechargeable power systems to support industrial energy storage and electric mobility.

Key regions are differentiated by their focus on specific battery performance metrics, such as extending cycle life in utility-scale applications or boosting energy density for consumer electronics.

This regional specialization shapes the global supply of secondary battery technologies and their components.

Market Dynamics

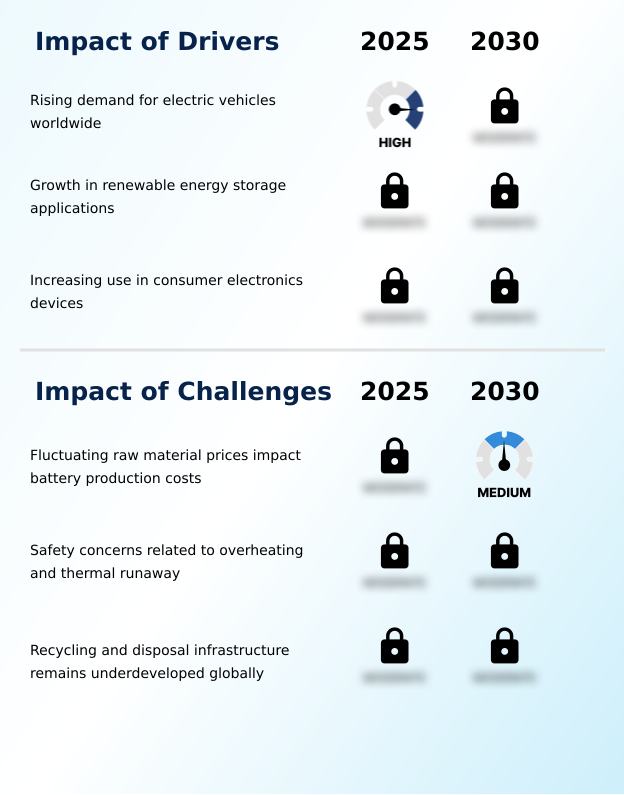

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A detailed analysis of advancements in high energy density battery cell development reveals a market intensely focused on performance gains for electric mobility and electronics. However, the impact of raw material prices on battery production remains a significant variable influencing cost structures across the industry.

- The secondary battery market segmentation by technology highlights the ongoing competition and distinct use cases when making a comparison of lead acid and lithium ion technologies. Concurrently, the secondary battery market segmentation by application shows how tailored solutions are created for automotive, industrial, and portable uses.

- Key strategies for improving battery reuse efficiency are becoming integral to corporate sustainability goals, though significant challenges in developing battery recycling infrastructure persist globally. The fundamental role of secondary batteries in renewable integration cannot be overstated, as they are essential for grid support.

- Innovations in thermal management for battery safety and optimizing battery management for extended cycle life are top R&D priorities. Furthermore, developments in solid state battery for electric vehicles and advancements in silicon anode lithium ion technology promise transformative changes. Secondary battery applications in industrial automation and understanding the growth factors for portable battery technologies reveal niche opportunities.

- Analysis shows that residential energy storage adoption trends are accelerating, while commercial peak load management with batteries offers clear ROI. Utility scale energy storage for grid support and trends in ess battery systems for commercial use are governed by evolving secondary battery safety standards and regulations.

- The economic viability of battery material recovery is improving, with some advanced processes showing a 20% higher yield in valuable materials compared to older methods, directly influencing supply chain strategies.

What are the key market drivers leading to the rise in the adoption of Secondary Battery Industry?

- The rising demand for electric vehicles worldwide is a primary driver for the market, accelerating the need for high-performance rechargeable batteries.

- Market growth is fundamentally driven by the accelerating electric vehicle adoption and the integration of renewable energy storage. The demand for lithium ion batteries is surging, underpinning the expansion of battery energy storage systems that are crucial for grid stability.

- These energy storage solutions range from utility scale battery storage projects to decentralized energy storage in commercial buildings, improving energy resilience by 30%. The proliferation of consumer electronics devices further fuels demand.

- Meanwhile, breakthroughs like silicon anode lithium ion technology are enhancing performance, making electrification more viable across all sectors and applications.

What are the market trends shaping the Secondary Battery Industry?

- Advancements in solid-state battery technology development represent a significant trend. The industry is moving toward safer and more efficient energy storage solutions.

- Key trends are shaping the future of high performance energy storage, with a significant push toward solid state battery development. These advanced energy storage systems promise enhanced safety and higher energy density, transforming applications from ev battery systems to portable energy solutions.

- Innovations in cell chemistry, such as improved lithium iron phosphate formulations, are enabling fast charging batteries that meet consumer expectations. The adoption of home energy storage systems is also accelerating, with these units becoming 25% more compact while offering the same capacity. This shift reflects a market-wide demand for more efficient and safer technologies.

What challenges does the Secondary Battery Industry face during its growth?

- Fluctuating raw material prices present a key challenge, directly impacting battery production costs and market stability.

- Significant challenges persist, particularly concerning the battery supply chain and volatile battery manufacturing costs. Mitigating the risk of thermal runaway through advanced thermal management systems remains a top priority, as incidents can undermine consumer confidence.

- The infrastructure for battery recycling and effective battery material recovery is still maturing, creating bottlenecks for ess battery systems and lithium ion polymer batteries used in industrial energy storage. Effective battery management systems are critical, not only for safety but also for maximizing efficiency, with advanced systems reducing energy waste by up to 15% during charging cycles.

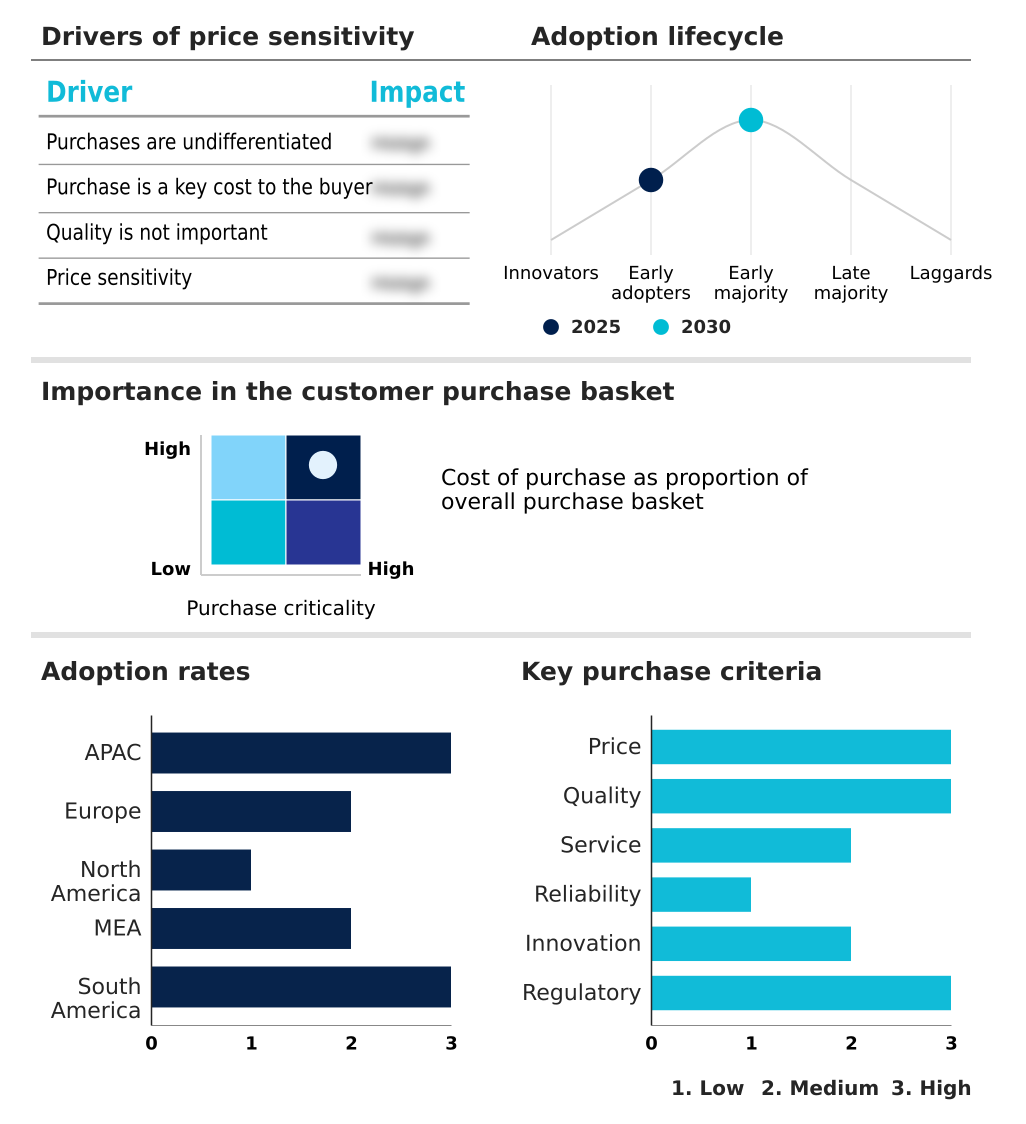

Exclusive Technavio Analysis on Customer Landscape

The secondary battery market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the secondary battery market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Secondary Battery Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, secondary battery market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

A123 Systems LLC - Offerings include advanced lithium iron phosphate batteries and modular systems, pivotal for high-performance energy storage applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A123 Systems LLC

- AESC Group

- Alliance Francaise d Atlanta

- Amprius Technologies Inc.

- BYD Co. Ltd.

- CALB Group Co. Ltd.

- CLARIOS LLC

- Contemporary Amperex Ltd.

- Discover Battery

- EnerSys

- EVE Energy Co. Ltd.

- GS Yuasa International Ltd.

- LG Energy Solution Ltd.

- Lithium Werks

- Murata Manufacturing Co. Ltd.

- Northvolt AB

- Panasonic Holdings Corp.

- Samsung SDI Co. Ltd.

- Toshiba Corp.

- VARTA AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Secondary battery market

- In March, 2025, Albemarle Corporation highlighted continued volatility in lithium prices due to shifting global demand and supply imbalances, impacting battery manufacturing costs across industries.

- In June, 2025, Redwood Materials announced expansion plans for its battery recycling operations to address growing volumes of end-of-life lithium ion batteries and improve material recovery efficiency.

- In July, 2025, Samsung SDI announced advancements in high energy density battery cell development aimed at improving fast charging performance and extending battery life for electric vehicles and consumer electronics.

- In September, 2025, Apple reported increased production of next generation devices with improved battery efficiency and optimized energy consumption systems, reflecting the continuous demand for advanced secondary batteries in consumer electronics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Secondary Battery Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 27.3% |

| Market growth 2026-2030 | USD 52561.8 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 21.5% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- From a research perspective, the market is defined by the interplay between various secondary battery types, from legacy lead acid battery systems to advanced battery technologies. The push for high energy density is relentless, driving innovation in cell chemistry for both lithium ion batteries and emerging solid state battery concepts.

- Battery management systems are increasingly sophisticated, crucial for optimizing cycle life and preventing thermal runaway. In the automotive sector, solutions range from traditional automotive lead acid batteries to advanced prismatic lithium ion batteries and silicon anode lithium ion formats. For stationary applications, battery energy storage systems, including ess battery systems, are fundamental for grid stability.

- The evolution of lithium iron phosphate and lithium ion polymer batteries continues to expand application possibilities. A critical boardroom consideration is the lifecycle of these assets; with battery recycling now achieving over 90% material recovery in some streams, it is becoming a mandatory component of sustainable operational planning.

What are the Key Data Covered in this Secondary Battery Market Research and Growth Report?

-

What is the expected growth of the Secondary Battery Market between 2026 and 2030?

-

USD 52561.8 billion, at a CAGR of 27.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Lead-acid, Lithium-ion, and Others), Application (Automotive batteries, Industrial batteries, Portable batteries, and Others), End-user (Residential, Commercial, Industrial, and Utilities) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for electric vehicles worldwide, Fluctuating raw material prices impact battery production costs

-

-

Who are the major players in the Secondary Battery Market?

-

A123 Systems LLC, AESC Group, Alliance Francaise d Atlanta, Amprius Technologies Inc., BYD Co. Ltd., CALB Group Co. Ltd., CLARIOS LLC, Contemporary Amperex Ltd., Discover Battery, EnerSys, EVE Energy Co. Ltd., GS Yuasa International Ltd., LG Energy Solution Ltd., Lithium Werks, Murata Manufacturing Co. Ltd., Northvolt AB, Panasonic Holdings Corp., Samsung SDI Co. Ltd., Toshiba Corp. and VARTA AG

-

Market Research Insights

- The market's dynamics are shaped by key demand drivers, including widespread electric vehicle adoption and the growth of renewable energy storage. The need for high performance energy storage is driving investment in energy storage infrastructure, from utility scale battery storage to decentralized energy storage solutions.

- For industrial battery solutions and ev battery systems, optimized thermal management systems can improve efficiency by 15%. The battery supply chain is under pressure to meet demand, with battery manufacturing costs being a critical factor. Innovations in battery material recovery are supporting battery reuse solutions and improving the economics of rechargeable power systems.

- Home energy storage systems and portable energy solutions for consumer electronics devices also represent significant segments, where battery performance metrics are key. Overall, advanced energy storage technologies are enabling a transition toward more resilient power systems, reducing reliance on traditional uninterruptible power supply setups and enhancing power grid stabilization.

We can help! Our analysts can customize this secondary battery market research report to meet your requirements.

RIA -

RIA -